In the current financial ecosystem, personal cheques continue to spark debate as digital payments gain popularity. Print & Cheques Now Inc. (chequesnow.ca) has long championed secure, reliable cheque printing services for Canadian business owners, accountants, lawyers, and other professionals. Although digital payments offer immediate, automated processing, personal cheques retain relevance in many business contexts. This article examines historical usage, current benefits, and future trends as 2025 approaches. It contrasts personal cheques with digital payment alternatives, explores technological improvements in cheque processing, and evaluates both domestic and global trends. The discussion provides a detailed perspective for financial printing experts and decision makers who value secure, well-documented payment procedures.

Transitioning to the main content, the following sections discuss how historical and modern cheque practices inform current operations, compare digital payments with cheques, review technological innovations, outline future trends, present international comparisons, and evaluate modern payment alternatives.

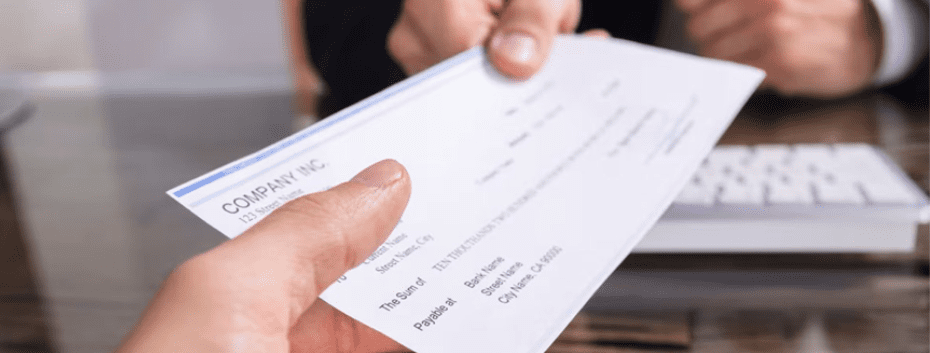

Understanding the Role of Personal Cheques in Modern Transactions

Personal cheques have long been a trusted payment method. Initially used when paper-based instruments were the norm, they offer lasting benefits such as traceability, record keeping, and serving as legal evidence in disputes. Their continued use is supported by the familiarity and trust developed by long-standing business owners and traditional financial institutions.

Define the Historical Use of Personal Cheques for Payments

Personal cheques were once the primary method for transferring funds between individuals and businesses. Handwritten and used to settle debts or pay for goods, each cheque acted as an informal contract between parties. Their widespread use helped standardize banking practices and recordkeeping. Even after electronic alternatives emerged, physical cheques provided tangible records that could be archived for audits and legal review.

Examine the Current Benefits of Using Personal Cheques

Today, personal cheques provide inherent security and traceability. Their design includes watermarks, signature panels, and unique numbering systems that deter fraud. Business owners appreciate the verifiable audit trail cheques create through a methodical clearance process. Unlike many digital channels involving third parties, cheque payments allow direct bank-to-bank processing, reducing digital breach risks and offering more control over large-value transactions. For sectors requiring detailed recordkeeping, cheques also support thorough internal auditing and regulatory compliance. Learn more about the benefits of having personalized cheques and how they can enhance your business security and efficiency.

Identify Typical Scenarios Where Cheques Remain Preferred

Many transactions still favor personal cheques. For example, business-to-business payments, rent, and invoice settlements often require a documented paper trail for legal compliance. Certain industries and professionals—such as law firms, construction companies, and government contractors—prefer cheques due to their emphasis on security and accountability. These reliable, periodic payments fit into enhanced payment routines safe from the uncertainties of digital methods.

Analyze Age Demographics Using Personal Cheques Today

Older generations and established companies continue to use personal cheques actively. Studies show that individuals aged 55 and over are much more likely to use paper cheques compared to younger groups. This trend highlights that familiarity offers comfort and efficiency. The steady use by older demographics ensures that cheque processing remains an essential part of the financial landscape.

Investigate Trust and Familiarity With Cheque Payments

Trust in personal cheques remains strong. Many business owners view them as secure and predictable, reducing the likelihood of disputes. The straightforward verification process reinforces consumer confidence. Compared to digital payment methods, which can face issues such as data breaches and cyber fraud, the traditional paper-based approach provides clear, verifiable documentation that appeals to longstanding financial institutions. For those who value this trusted payment method, it’s easy to order personal cheques from reliable providers offering secure and customisable options.

Analyzing Digital Payments Versus Personal Cheques in 2025

As the financial industry increasingly digitizes, it is important to compare the security, accessibility, and reliability of digital payments with personal cheques. Digital payments offer speed, convenience, and seamless integration with modern accounting systems. However, cheques continue to appeal because of their traceability and simple, effective verification processes.

Compare the Security Features of Digital Payments and Cheques

Digital payments use encryption, multi-factor authentication, and fraud monitoring, yet can be vulnerable to sophisticated cyberattacks. In contrast, personal cheques enhance security through features like watermarks and bank validation processes with physical verification. This tangible evidence makes it easier to document and challenge fraudulent transactions.

Discuss Accessibility of Digital Payment Methods Versus Cheques

Digital payments are highly accessible, requiring only a smartphone or computer and an Internet connection. However, they may alienate users in rural areas or older demographics uncomfortable with rapid technological changes. Personal cheques, which need little technological infrastructure, provide an alternative for businesses used to traditional banking practices.

List Industries Still Relying on Personal Cheques Primarily

Industries such as real estate, legal services, government contracting, and professional services often rely on cheques. These fields value the established nature of paper cheques for their detailed recordkeeping and legal enforceability. Many organizations have integrated cheque processes into refined internal accounting systems, ensuring that cheques remain a pivotal tool for high-stake transactions.

Identify Potential Issues With Reliance on Digital Payments

Although digital payments offer faster processing, they are susceptible to issues such as technical glitches, cyber threats, and privacy concerns. Dependence on constant connectivity means digital systems can fail during unforeseen outages. Businesses that rely exclusively on digital payments risk exposure to rapid technological failures, which is why some prefer to maintain cheque-based alternatives as a safeguard.

Highlight Users’ Sentiments Towards Both Payment Methods

User opinions are divided between the convenience of digital transactions and the traditional reliability of cheques. Business owners who have resolved disputes with the clear paper trail of a cheque often favor a hybrid approach. Surveys among Canadian professionals indicate that while digital transactions are popular for everyday use, many still prefer cheques for larger sums or formal contracts because of the added peace of mind.

Exploring Technological Innovations Affecting Personal Cheques

Recent advances in financial technology are reshaping traditional cheque processing. Innovations aim to improve the speed, accuracy, and security of cheque transactions, ensuring that personal cheques remain competitive in a digital age.

Investigate Cheque Verification Technology Advancements

Modern systems now use real-time validation and artificial intelligence to detect discrepancies in signatures and handwriting. These advancements reduce human error and enhance security by flagging potentially fraudulent transactions before clearance. Banks are increasingly using machine learning algorithms to integrate cheque data into secure databases, streamlining processing for business cheques.

Analyze Developments in Cheque Imaging and Processing

Cheque imaging technology has greatly reduced manual processing times and errors. High-resolution scanners and optical character recognition software enable banks to quickly digitize cheques while preserving the original document for legal reference. This helps bridge the gap between traditional cheque use and digital systems, speeding up fund confirmation while lowering overhead costs.

Examine the Impact of Fintech Solutions on Cheque Use

Fintech innovations continue to modernize cheque payments by linking them with digital banking platforms. For example, software now allows users to deposit cheques remotely via mobile apps, negating the need for in-person bank visits. This integration not only saves time but also boosts overall cheque security as data is promptly encrypted and verified.

Discuss Mobile Banking Apps Supporting Cheque Functionalities

Mobile apps have advanced to support cheque management and deposit functions. Users can capture cheque images, verify amounts, and monitor clearance status directly from their smartphones. This increased accessibility benefits small businesses and finance officers, boosting efficiency and reducing processing errors through real-time tracking.

Identify Software for Easier Cheque Management for Users

Innovative cheque management software now streamlines an entire cheque’s lifecycle. These platforms offer automated recordkeeping, reconciliation tools, and integration with enterprise resource planning systems. Such systems enable businesses to manage cheque issuance, monitor outstanding payments, and generate detailed audit reports, ensuring cheques continue to serve as a vital transaction method in 2025.

Evaluating Future Trends in Personal Cheque Usage

The future of personal cheques will likely mirror changes in technology and consumer behavior. Although digital payment methods are growing, several factors indicate that cheques will endure, especially in high-value or legally sensitive transactions.

List Trends Indicating a Rise or Decline in Cheque Acceptance

Recent trends suggest that while cheque usage in everyday transactions is declining, business and legal sectors still depend on them for high-value, record-sensitive operations. Regulatory requirements, legacy accounting practices, and the need for documented payment trails contribute to this sustained acceptance. In fact, enhanced security measures and digital integration are making cheques more efficient than ever, potentially fostering a modest resurgence in niche markets.

Discuss Demographic Shifts Influencing Cheque Usage

As older generations who traditionally used cheques retire, overall usage may seem set to decline. However, this decrease is partially offset by businesses and older professionals who continue to prioritize the clarity and accountability cheques provide. Some emerging markets even adopt a hybrid approach, using cheques where digital infrastructure is less developed. This balance helps maintain cheque relevance despite shifting demographics.

Identify Potential Regulatory Changes Affecting Cheques

Regulatory frameworks are continually updated to boost financial security and consumer protection. Future policies may impose stricter verification standards for digital payments, which could inadvertently reinforce the use of paper cheques for high-value transactions. Canadian regulators, for example, might introduce guidelines that enhance transparency in cheque processing, further cementing their role in compliance and audit practices.

Analyze the Role of Personal Cheques in Job-Related Transactions

For many contractors, consultants, and vendors, personal cheques provide a dependable payment method. Their legally binding nature helps businesses enforce contracts and maintain clear financial records. Whether used to settle invoices or for payroll in small businesses, cheques facilitate transparency and help reduce internal disputes.

Consider Factors Leading to a Potential Resurgence of Cheques

Several elements might encourage a moderated comeback in cheque usage. Advances in processing technology, coupled with skepticism about the security of purely digital transactions, create a niche where cheques remain attractive. Businesses that value secure, verifiable payments may view cheques as a reliable alternative amid concerns over digital payment vulnerabilities. As Print & Cheques Now Inc. continues to innovate, improved cheque services could draw a new generation seeking the blend of tradition and modern functionality.

Learning From International Perspectives on Personal Cheques

International trends reveal a varied acceptance of cheque payments, shaped by cultural and regulatory factors. By examining practices in different countries, Canadian business owners can understand how traditional cheque methods are maintained or adapted globally.

Compare Cheque Usage Rates in Various Countries

Countries with strong banking traditions—such as Canada, Germany, and Japan—tend to maintain higher cheque usage in specific business contexts compared to nations that favor digital payments. For example, in the United Kingdom and Australia, cheques serve niche markets even though digital payments dominate retail transactions. These comparisons highlight how legacy systems and supportive regulations can sustain cheque usage where digital transformation is less pervasive.

Discuss How Cultural Attitudes Shape Cheque Acceptance

Cultural attitudes strongly influence financial practices. In many European countries, cheques are seen as reliable instruments combining sentimental value with rigorous accountability. In contrast, nations that have rapidly embraced digital innovation may view cheques as outdated. Yet, even in highly digitized markets, the need for verifiable records in significant transactions helps preserve cheque acceptance. Overall, trust and tradition play as much a role as technology in determining cheque usage.

Examine Regulatory Influences on Cheque Transactions Globally

Global regulatory standards shape how cheques are processed. Countries with strict anti-fraud measures and transparent auditing practices typically favor cheque usage, integrating it into their broader financial ecosystems. In regions like the European Union, cheque verification is part of comprehensive regulatory frameworks that ensure both security and legal compliance.

Highlight Innovations in Cheque Processing Internationally

Internationally, advances such as real-time verification, electronic imaging, and even blockchain integration are setting new benchmarks for cheque processing. Several European banks have adopted advanced OCR systems alongside AI-driven fraud detection to confirm cheque authenticity. These innovations not only secure transactions but also create a seamless bridge between traditional and digital payment methods.

Identify Lessons From Countries Where Cheques Are Thriving

Experiences from markets like Canada and the United Kingdom demonstrate that cheques remain viable when combined with modern technology. Lessons show that by embracing technological integration, businesses can enhance transparency and legal validity while retaining the traditional benefits of cheques. This balanced approach offers a resilient model that other regions can follow.

Assessing Cheque Alternatives and Their Future Viability

Despite the enduring role of personal cheques, several modern alternatives are competing in the payments landscape. Evaluating alternatives such as digital wallets, cryptocurrencies, and prepaid cards helps to understand the evolving financial strategies of Canadian businesses.

List Common Alternatives to Personal Cheques Today

Common alternatives include digital payment platforms like Interac e-Transfer, mobile wallets such as Apple Pay and Google Wallet, cryptocurrencies, prepaid cards, and ACH transactions. While each option offers benefits like speed and convenience along with digital recordkeeping, they often lack the strong audit trail that personal cheques provide, making them less ideal for transactions needing detailed documentation.

Discuss Pros and Cons of Digital Wallets Compared to Cheques

Digital wallets allow for instant transfers and have high usability across devices; however, they can be vulnerable to cybersecurity risks and do not offer a physical record. Personal cheques, though slower, provide a tangible, legally enforceable record and are less prone to hacking. Depending on the transaction’s priority—speed versus security—business owners may prefer one method over the other.

Analyze the Impact of Cryptocurrencies on Cheque Relevance

Cryptocurrencies offer decentralized payments and lower fees but face challenges in regulatory acceptance and price stability. Although blockchain transparency is a plus, the lack of a conventional legal framework makes cryptocurrencies a riskier choice for routine business payments compared to the longstanding stability of cheque transactions.

Investigate How Prepaid Cards Are Replacing Personal Cheques

Prepaid cards offer a secure digital alternative increasingly used for managing corporate expenses and small purchases. They combine safety features with easy tracking, though they require electronic validation and often do not generate a detailed paper trail. For transactions where meticulous recordkeeping is critical, cheques still hold an advantage.

Identify the Future Outlook for Cheque Alternatives in 2025

While digital payment alternatives are expected to continue growing, the unique attributes of personal cheques—security, auditability, and legal enforceability—will ensure they remain relevant in specific sectors. A hybrid model, where routine payments are digital and high-stake transactions use cheques, is emerging as a secure and balanced strategy moving into 2025.

Summary Table of Payment Alternatives

Before proceeding, consider this table comparing key attributes of personal cheques and their alternatives:

| Payment Method | Security Feature | Processing Speed | Documentation Benefit | Typical Use Case |

|---|---|---|---|---|

| Personal Cheques | Watermarks, signature verification | Slow (2-3 days average) | Strong physical audit trail | High-value business transactions, legal docs |

| Digital Wallets | Encryption, two-factor authentication | Instant | Digital records (less tangible) | Retail payments, everyday P2P transfers |

| Cryptocurrencies | Blockchain transparency | Varies | Immutable ledger (non-standard) | International transfers, speculative exchanges |

| Prepaid Cards | PIN protection, fraud monitoring | Instant | Trackable, though not legal proof | Corporate expense management, small purchases |

| ACH Transfers | Bank-level verification | 1-2 business days | Electronic transaction records | Regular payroll, recurring invoices |

This table summarizes the strengths and limitations of each payment method. While personal cheques offer unmatched documentation and security in legal contexts, digital solutions excel in speed and convenience, supporting a hybrid financial strategy.

Final Thoughts

Personal cheques continue to hold their ground in the financial landscape of 2025. They offer unmatched security and documentation that digital payments sometimes lack, particularly for high-value or legally sensitive transactions. As technological innovations streamline cheque processing further, businesses are expected to adopt a hybrid strategy that leverages both traditional and digital payment methods. This balanced approach will help maintain robust financial accountability and trust in an increasingly digital world.

Frequently Asked Questions

Q: What makes personal cheques still relevant in 2025?

A: Personal cheques remain vital due to their strong audit trail, inherent security features, and legal enforceability, especially in high-value transactions. They are preferred by industries that value detailed recordkeeping and traditional banking practices.

Q: How do technological innovations improve cheque processing?

A: Advancements such as AI-driven verification, high-resolution imaging, and mobile deposit apps streamline cheque processing by reducing human error and enhancing security, thereby blending traditional methods with modern protocols.

Q: Are digital payments completely replacing personal cheques?

A: While digital payments are popular for everyday transactions, personal cheques remain essential in sectors that require verifiable documentation and legal proof. A hybrid payment model is emerging where both methods coexist.

Q: What are the key benefits of using personal cheques over digital methods?

A: Cheques provide enhanced security through physical verification, offer traceable audit trails, and serve as legally binding documents. These benefits make them ideal in industries like legal services, real estate, and government contracting.

Q: How will future regulatory changes impact cheque usage?

A: Expected regulatory updates may impose stricter verification for digital methods, thereby indirectly supporting cheque usage by reinforcing transparency and detailed recordkeeping in high-stake transactions.

Q: Which industries continue to predominantly use personal cheques?

A: Sectors such as legal services, real estate, construction, and government contracting continue to use cheques due to their need for detailed financial records and security in transactions.

Q: Can small businesses benefit from maintaining cheque payment options?

A: Yes, small businesses benefit from cheques through clear, documented transactions that support internal audits and ensure legal compliance. Cheques are a secure alternative for handling high-value invoices and formal contracts.